Flames Financial Dashboard

Free Household Cash Flow Planner

Create an annual household cash-flow plan without categorizing every transaction. Organize income, estimated taxes, savings, fixed expenses, flexible spending, and remaining surplus or shortfall.

Direct answer

How Can I Plan Annual Cash Flow Without Tracking Every Transaction?

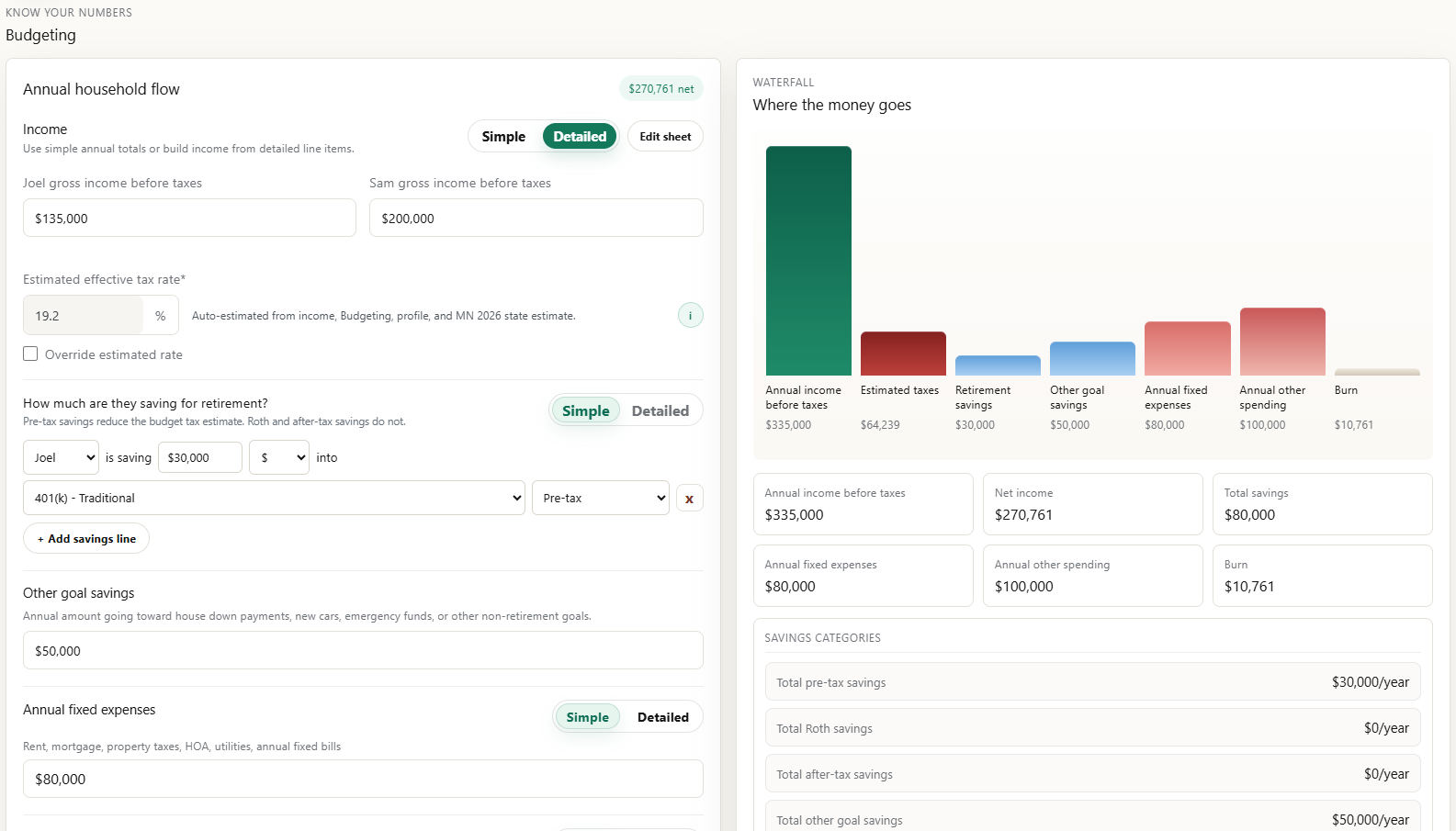

Use a household cash-flow plan: gross income minus estimated taxes, savings, fixed expenses, and flexible spending equals the remaining surplus or shortfall.

You do not need perfect transaction categorization to make better planning decisions. Start with annual totals, estimate the big categories, and refine only the areas that change the answer. The Flames Financial Dashboard supports simple annual inputs and more detailed worksheets when a household needs more precision.

Formula

The Household Cash-Flow Formula

This is the planning math behind the page. It is meant to make decisions visible, not to turn every receipt into a permanent chore.

How to build it

Start With the Big Categories Before You Add Detail

A cash-flow plan is most useful when it shows the pressure points: taxes, savings, fixed commitments, flexible spending, and whether the plan is sustainable.

Cash-flow inputs

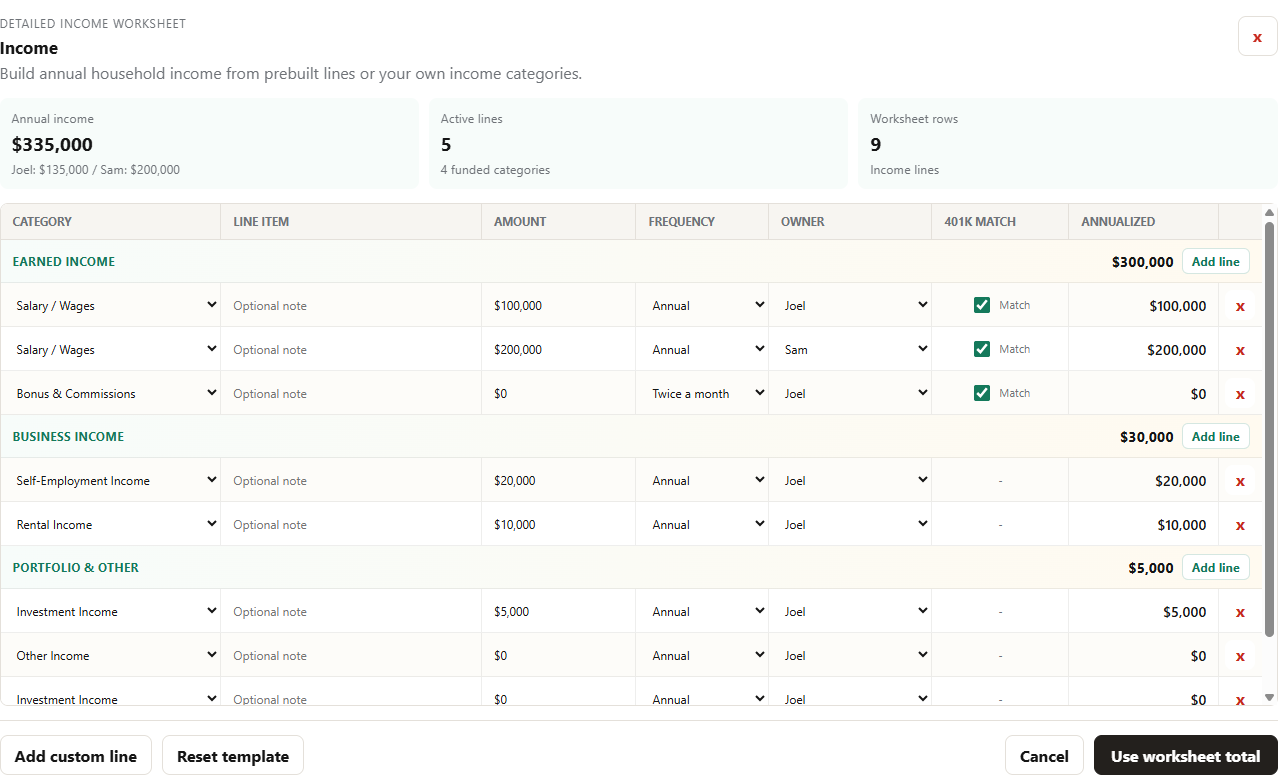

- Salary, bonus, commissions, business income, rental income, investment income, pensions, Social Security, and other income.

- Estimated federal, state, payroll, and other tax assumptions.

- Retirement savings and other goal savings.

- Fixed expenses such as housing, debt payments, insurance, childcare, utilities, and subscriptions.

- Flexible spending such as groceries, restaurants, travel, clothing, entertainment, and personal care.

Use annual totals first

If the goal is planning, annual totals often matter more than exact category history. Start with the big number, then refine the category that creates uncertainty.

Separate fixed from flexible

Fixed expenses show commitments. Flexible spending shows the area that can usually change fastest if savings or debt payoff need more room.

Connect savings to goals

Retirement savings, emergency fund savings, child savings, and debt payoff should connect to a goal, not disappear into a generic savings bucket.

Examples

What Cash-Flow Planning Helps You Decide

Can we afford a larger retirement contribution?

Compare the current savings rate, estimated tax impact, fixed expenses, and the remaining annual surplus before increasing contributions.

Should extra cash go to debt or savings?

Review the emergency fund, debt rate, minimum payments, payoff timing, and whether the cash is needed for upcoming goals.

Are we overspending or under-saving?

The dashboard separates income, taxes, savings, and expenses so the gap is easier to see than it is inside monthly transactions.

What should we bring to an advisor?

Bring the cash-flow snapshot, goals, debts, and open questions when tax, retirement, investment, estate, insurance, or competing-goal decisions need judgment.

Related dashboard guides

Use Cash Flow With the Rest of the Dashboard

Net worth tracker

Use assets and liabilities to see the household balance sheet behind the cash-flow plan.

Open net worth trackerFinancial goals

Assign planned savings to retirement, child savings, emergency fund, debt payoff, and future purchases.

Open goal plannerYNAB or Rocket Money companion

Use a transaction app for daily detail and the dashboard for annual planning.

Compare the toolsThe Flames Financial Dashboard is an educational planning tool. It is not financial, tax, legal, or investment advice. Tax and cash-flow calculations are planning estimates and do not replace personalized professional advice.